Greece: Indices of residential property prices Q3 2025

- 3 December, 25

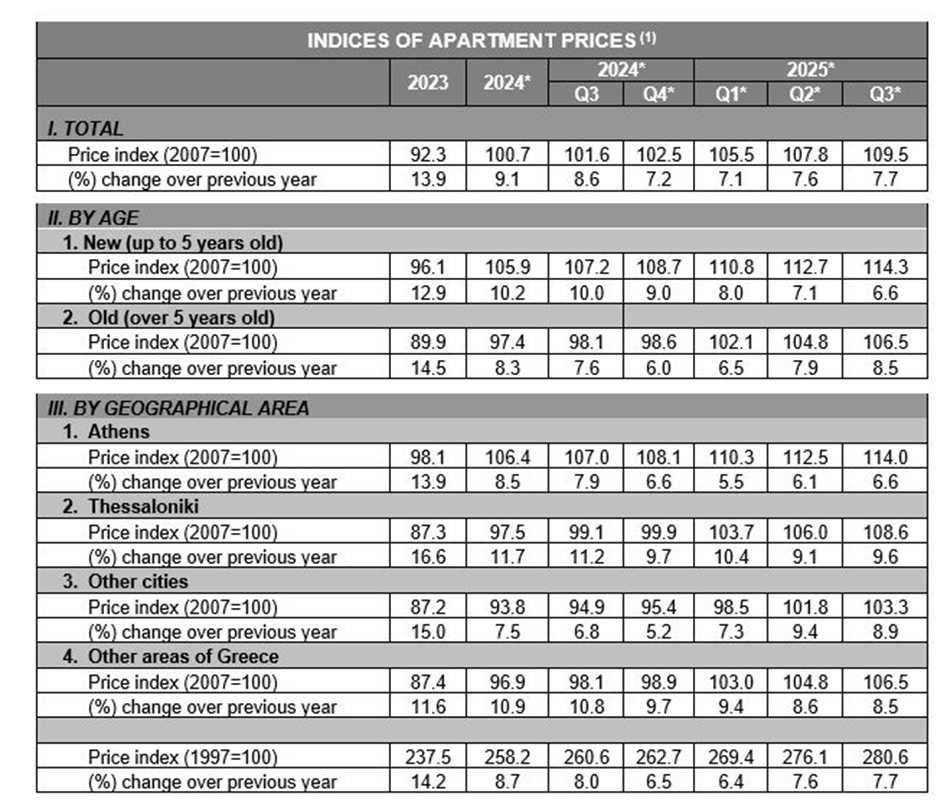

According to the Bank of Greece’s November 2025 Report, the Indices of Apartment Prices recorded by 7.7% in 3Q2025. During the first three quarters of 2025, apartment prices rose by 7.1%, 7.6%, and 7.7%, respectively. This trend indicates that after the sharp slowdown in 2024, the market is now entering a phase of mild but stable deceleration. Solaya forecasts that Q4 2025 growth will remain above 7%, bringing the full-year 2025 average increase to approximately 7.4%, signaling a sustainable recovery.

In Q3 2025, new apartments (under 5 years old) rose 6.6%, while older apartments (over 5 years) outperformed significantly with an 8.5% increase. This reflects the strong investor demand for older units, especially in central districts and areas with convenient transportation.

The ongoing renovation wave involving old shops and former office spaces in Athens is also helping ease housing supply pressure while delivering attractive returns. Combined with the nationwide data showing stronger price growth in older units, this trend continues to support stable real estate appreciation. For homebuyers and investors, older apartments in central locations and redevelopment projects remain key investment opportunities.

From 2023 to Q3 2025, the market experienced a notable shift. After a steep 4.8-percentage-point drop in price growth during 2024 (from 13.9% to 9.1%), the slowdown in 2025 is expected to narrow to just 1.7 percentage points by year-end. This indicates a more positive and stabilizing outlook for Greece’s residential property market.

Athens’ old shops, offices find new life amid housing crunch, investor demand

Between the 1950s and 1980s, many newly built residential buildings included two to three ground-floor retail units. Most were retained by developers or sold to independent investors—meaning these commercial spaces are typically not owned by apartment residents, adding complexity in building management. The financial crisis further weakened the viability of small retail units and offices, especially those with limited foot traffic. Many became vacant for long periods or operated with low profitability.

A similar situation is seen in hundreds of small offices in central Athens. As demand for office rentals declined, owners increasingly opted to sell or convert them into residential units. Although these offices were not originally designed for housing, their prime central locations make them a practical solution to ease housing shortages.

In the past year alone, office prices in central Athens surged 17.3%, reaching an average of €2,167/m². This demonstrates strong buyer interest and highlights the substantial potential for conversion into apartments or even full residential buildings, unlocking significant investment value.

Cre: Ekathimerini